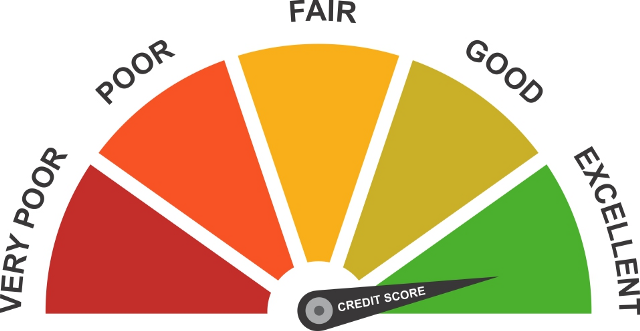

A credit history containing unfavorable comments, such as late payments or charged-off accounts, may negatively impact a person's credit score. This is what is meant by the term "bad credit." According to myFICO, a credit score is considered low or terrible if it falls below 300 and 579 out of a potential 850 points. No predetermined period can be used to estimate how long it will take to fix errors made on your credit report and raise your score into the "good credit" area, defined as a FICO score of 670 or above. It is contingent on a variety of elements, including the following:

- The specific types of errors that might be found on your credit report.

- How many marks considered bad or derogatory marks might be seen on your credit report?

- An era dominated by unfavorable information

- The previous score of your credit rating before it began to decline.

The difficulty of the bad history that is weighing down your score may determine how long it takes for you to recover your credit. For instance, it could be more difficult to recoup losses through a charge-off, foreclosure, bankruptcy, or court judgment than it would be from a single overdue payment.

- Every overdue payment includes: As much as seven years

- Charge-off: Anywhere from one to seven years

- Up to seven years for bills that have been turned over to collection agencies

- Accounts that have been settled: up to seven years

- Accounts that have been closed for up to ten years

- Up to Seven Years for a Foreclosure Process

- Filings under Chapter 7 of the Bankruptcy Code: Up to Ten Years

- Up to two years for difficult inquiries made while applying for new credit

Reporting the first late or missing payment might result in removal from the program. Check your credit report to see when a bad item will be removed from your credit history. The date may be seen on the report. The credit reporting agency providing the negative information will identify the month and year when it will be erased. In principle, a person with an excellent FICO credit score of 800 or more may have a longer wait period to return to the excellent credit range if their score drops into the terrible credit area. On the other hand, if you had a good credit score (from 580 to 669 points) before it dropped, it may not take as much time for it to rise back up from the range of poor credit to the range of good credit again.

Obstacles in the Way of Repairing Damaged Credit

Five different things might have an effect, either good or bad, on your credit score. Each one contributes a certain amount to your overall FICO score.

- Payment history accounts for 35%: Make on-time payments of the whole amount due for bills.

- Amounts that are still owing (30%): Reduced balances and a lower level of utilization

- Length of credit history accounts for 15% of the score: Don't cancel down your previous accounts; rather, utilize the ones you have now.

- Inquiries about obtaining new credit (ten percent): If it's not required, you should refrain from applying for new credit.

- Credit mix (10%): Make use of a variety of credit options, including loans, credit cards, and more.

After a hiccup in your credit history, you may rebuild a positive credit history by demonstrating responsible behavior in the following five areas. While your creditors are not compelled to report the activity on your accounts to the credit agencies, they almost always do so since it serves their business interests. They might carry out this activity once or every other month, depending on how well it fits into their schedule.

However, one month of good behavior, such as decreasing a debt level, may not be enough to wipe out the effects of many months of missing payments or something more severe, such as filing for bankruptcy. Establish your creditworthiness by demonstrating a track record of responsible credit usage. It may be many months before you notice any substantial changes in your credit ratings.

Alternative Methods for Repairing Damaged Credit

Although getting a credit card may be one of the most effective ways to improve a poor credit rating, there are other options available to you that also have the potential to improve your score. Be sure to consider and assess all of your choices before attempting to restore your credit, including the following:

- A credit builder loan may be obtained from your bank or credit union.

- A personal loan of lower amounts often requires a co-signer. (You can find out how much you'll have to pay back for a personal loan using the calculator provided below.)

- A credit card issued by a retail business, for which approval with a lower credit score could be simpler to get.